I really love Lyn Alden for her great write-ups. Her tireless and relentless pursuit of Bitcoin truths, and naturally the fact that she came to almost the same conclusions about Bitcoin as are most compatible with ancient Bitcoiner understanding is very rare: either she is a goddess in terms of digging up high-quality information (my current assumption,) or someone with an ancient Bitcoin understanding is very carefully supplying otherwise heavily obscured information to her over time. Typically new people are bombarded by the lies and massive self-referential echo chambers that Bitcoin attackers have been building for 8 years or more and based on experience it's difficult even for extremely intelligent and capable people to avoid mistakenly integrating at least a few of these lies over time.

Also, it's been very helpful for Lyn to make Bitcoin truths stick in other peoples' heads: I no longer need to repeat so many things ad nauseum, because her charisma is significant and people believe her.

Thus, it's painful for me to beat my old there-is-no-market-cap drum again. But.. there is no Bitcoin market cap.

The idea of a Bitcoin Market cap is old—very old in Bitcoin terms—but as far as I can tell it either originated with or was at least widely popularized by Trace Mayer, who applied the idea of a stock's market cap to the combined value of all gold in the world, and then likened Bitcoin to that, and began making the claim widely in public.

However, there's no such thing for any kind of money, nor really any commodity. It overestimates the size of bitcoin specifically because it implies that large amounts of it could be converted at current prices; it ignores the actual size of the Bitcoin economy as a measure which is actually much smaller than the market cap implies; and it limits the price growth in peoples' minds to an artificial cap based on how "much" of the world's wealth is captured in Bitcoin's market cap, when it clearly isn't.

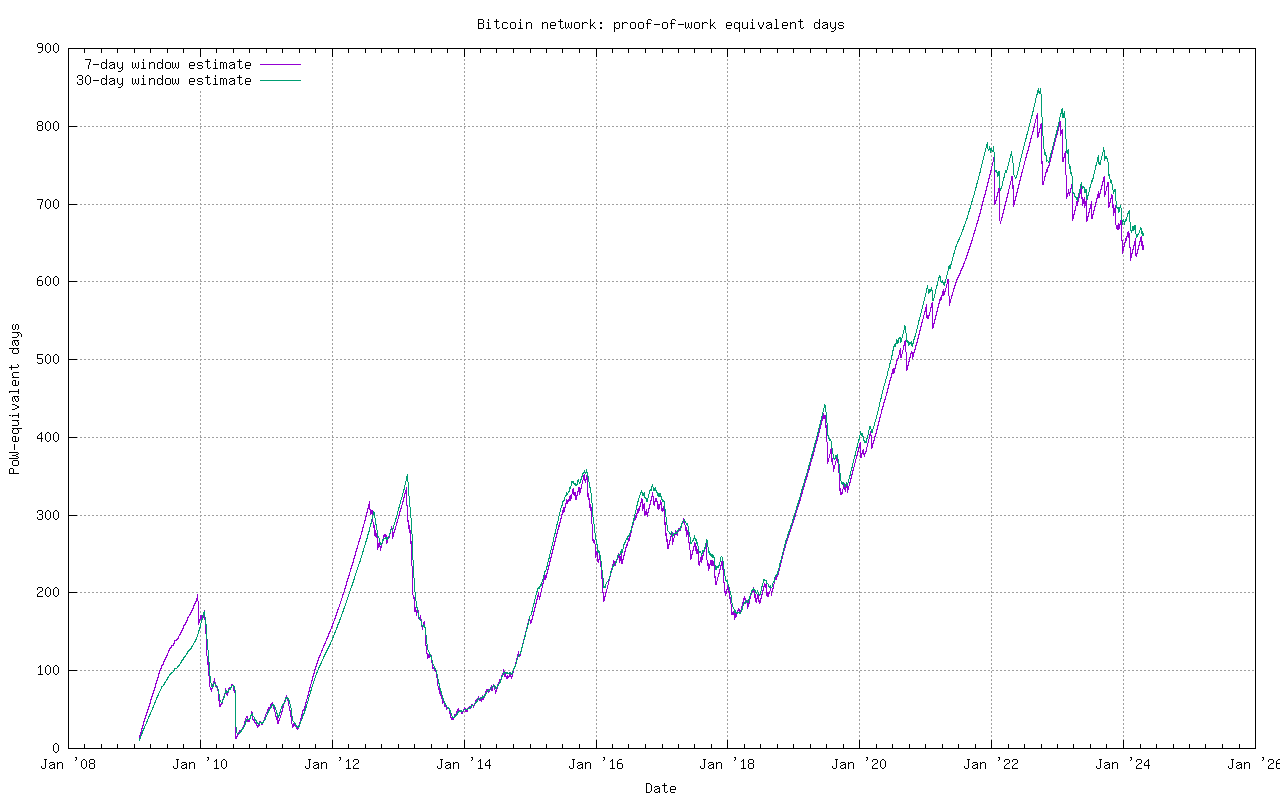

Partly this has to do with the fact that the price has risen significantly over the last decade—but are Bitcoins that someone paid or mined for $0.20 in November 2010 actually fully worth $46,000 USD today? Did we put the equivalent of $46,000 into the Bitcoins from 2010 in equivalent measure to the coins we put into mining today that miners have to sell at in order to pay for their operations? Obviously not, and neither did stock-owners who bought Apple—but when people buy Apple stock, they have full financials with regards to Apple's performance and the entire company maintains careful metrics. There is no such thing for Bitcoin. All we can do is guess. In Bitcoin's case reasoning about this is complicated by the fact that Bitcoin's miners pile work approximately valued at the price they require to continue operating, on top of all old Bitcoins—and obviously the (less than perfect) fungibility of Bitcoin means these are usually interchangeable, but the point is, the current prices of Bitcoin were not the prices of Bitcoin until very recently. Total economic value of work piled into Bitcoin also changes slightly as miners become more efficient: a really good representation of this is at sipa's interesting PoW-days equivalent work graph here.

{kind=link}

More annoyingly, market cap also is a measure which can be trivially manipulated, though less so in Bitcoin's case. We could issue a token tomorrow and if we issue a trillion of them, and then I sell one to you for $1,000, does that mean we have a $1 quadrillion dollar market cap? Obviously in that case the measure is meaningless. Why then do we assume it has the full value of the market cap with Bitcoin, which was in its nascence less than pennies? It seems more logical to realize that the answer is somewhere currently unknown in between, and the measure itself is more of an illusory upper bound of the actual size of the economy that supports the price at its current valuation. To mock the idea itself of a market cap, some people have even created chains that have an infinite market cap. Obviously the world hasn't been swallowed by these.

Market capitalization is a stock term, and it is one which is only ever incorrectly applied to something like a commodity, or even a foreign currency. It is made-up as applied to Bitcoin, merely an analogy: Bitcoin is not a stock, neither is gold. Trace Mayer made up the notion that it applied to Bitcoin, I suspect, to help people understand that Bitcoin was a very strong asset going forward, and to pump its appearance of value in peoples' minds in order to convince them to take it seriously. This is no longer necessary. We should outgrow these outmoded training wheels.

If ethereum with its bizarre flexible and unknowable future supply "flips" Bitcoin, does that mean eth as an economy is also larger than Bitcoin's? Obviously, also no. Thus, reasoning based on market cap will always overestimate our (or ethereum's) economy's actual size, and underestimate our growth potential. It also overestimates our resistance to actual effective attack, and if ethereum ever does switch to proof-of-stake, obviously it will vastly over-estimate its resistance to effective attack.

If people think that Bitcoin's economy is somehow equal to its market cap, then when all those hodlers sitting on mountains of the stuff (collectively—I have indirect evidence that individual huge holders don't exist anymore) and our millions of users and friends worldwide collectively push the value of the market-traded amounts to some stratospheric value, say $150,000 or so, people will assume that $150,000 x 19,000,000 = $2,850,000,000,000 has been captured in the Bitcoin economy. This is likely simply not the case, but they will still decide what Bitcoin's upper value can be conceptually capped at and presume that Bitcoin price won't be able to reach much higher than that. There are memes about this already.

If, on the other hand, I'm right—and I do like being right, so I try hard at it—then in reality our economy which supports the current price is small enough that its growth can indeed push the price to actual additional stratospheric heights that will surprise even the skeptics.

I'll note just for the record, since people describing "stratospheric" prices have been mocked by distant descendants for calling it thus, I am merely describing it from the perspective of someone who has been sitting here watching it actively climb from $0.20 USD or so in fits and starts to what would have been utterly unthinkable in late 2010—its all-time high which as of this writing is $64,895 on Bitstamp. To me, it's already absurdly stratospheric, and I of course regret giving it away like water in the early 2010s, especially since almost 95% of all of those Bitcoins were simply lost.

And thus, since I think there is no Bitcoin market cap, my response to Lyn Alden's write up, which is linked here, follows below the link.

https://www.swanbitcoin.com/bitcoins-energy-usage-is-not-a-problem-heres-why-by-lyn-alden/ (archived as of August 11, 2021, here: https://archive.is/G82CT)

Each year so far, the Bitcoin network usually spent more on security than the year prior, but always spent a smaller percentage of its market capitalization on security than the year prior.

Bitcoin has no market cap: thus, its market capitalization is a false measure which in any event effectively acquires additional depth over time. Were the measure an accurate one (say, economy size or total to-exhaustion purchasing power) the point would likely be similar and probably correct; mining as a fraction of Bitcoin's economy's value has probably been shrinking. Certainly when I was solo-mining, a huge fraction of Bitcoin's economy was concerned with, and engaged in, mining as its primary bootstrapper.

By the 2030s, bitcoin miner revenue will probably be around 0.50% of market capitalization or less, and so the network will be stuck at 2018 – 2020 energy spending levels or less.

In the event that Bitcoin's price rises to stratospheric levels (and there's no real reason for it not to) then the amount of economic value pumped into mining will also increase as miners chase profits. The declining subsidy is a major enabler of significant price increases. To me, it seems the fee market which must develop will be the only way to truly unshackle the prices towards actual market value.

If Bitcoin becomes systematically important, let’s say $5-$10 trillion (representing a per-coin price of $250k to $500k)

Since Bitcoin has no market cap, then the price itself is not a direct implication of this value. Price itself is uncoupled from market cap based simply on the logic of the utility of a single unit, or a probabilistic fraction of that unit in Lightning, and the fact that most people are simply sitting on their Bitcoin. If price hits $100,000, this does not imply even that the economy itself has grown by a $100k/price_now multiple. Market cap implies too many incorrect things to be even a valuable measure by which to reason about this, as it's not even a static coefficient, but a variable one in time.

for a critically important market capitalization of $20 trillion, with billions of users

This is incorrect, as the mining incentives to reach profitability are directed towards meeting current price and current profitability, and predicted profitability. Any additional profitability above the cost of mining, as Luke-Jr is fond of correctly pointing out, will trend towards zero over the long term. If it is 3x electricity profit to mine as it approximately is now, then everyone can mine at a vast profit margin. This disconnect will eventually correct itself. This is also why a reduction in the subsidy acts as an unshackling which will allow a higher price to appear without significantly destroying the world's energy production by making it so profitable that everyone will mine instead of any other activity and the process becomes actually destructive.

We are currently subject to worldwide supply problems and silicon fabrication plant capacities as a friction to realizing full mining hashrate profit, and government frictions in places like China and elsewhere, where the absurdity of projected value judgements of energy use are becoming more or less fashionable.

Whether blocks are full or not, they’re using roughly the same amount of energy.

Not only that, but the miners are also adding additional security onto all past transactions over time. The real cost of a current transaction, on a long enough timeline, is potentially infinite, which is partly but certainly self-evidently why the logic around the costs of a single transaction are absurdities from any angle you look at it.

Whether you choose to make a transaction or not does not materially change how much energy the Bitcoin network is using at that time.

This would only be an implied true statement if the amount of transactions in a block were flexible and unlimited—since you don't have a choice to add additional transactions to the next block if it is full unless you're willing to bid higher than the lowest fee and compete with someone else's choice. This is not strictly possible, because the system becomes unstable with an unlimited block size unless the subsidy is permanent.

Plus, the second part is true only in the present. In the event that too few people choose to use Bitcoin, eventually mining hashrate will decrease as the value in Bitcoin will decrease in that hypothetical (it has in the ancient past, though the chances now are much lessened.)

which mainly comes from people holding bitcoin as a store of value, not spending it.

I would have said that a robust use of Bitcoin is from whence it derives its value in the past. "A weapon unused, is a useless weapon." (-General Sline, 1985) Realistically once adoption reaches some certain point it won't matter that the proportion of holders is unusually vast compared to its on-chain users.

which mainly comes from people holding bitcoin as a store of value, not spending it.

If everyone held at the beginning and nobody spent it, it likely wouldn't have been possible for the market to price-discover, and adoption would have been essentially nil.

Currently, exchange activity and action is resulting in a massive exodus of coins from exchange vaults. This is caused by large acquisitions of Bitcoin, plus the realization that current exchanges are a systemic risk to Bitcoin. To own your own Bitcoin, you must own it yourself. As the old saying goes, "No, Neo, I'm trying to tell you that when you're ready... you won't have to."

If transaction fees are averaging $1 for the base layer because block space isn’t been heavily used, for example, then $100 amounts are fine (isn't being—just a spelling error here)

On top of that, multiple layers ranging from trustless Lightning, to semi-trusted Liquid, to fully-trusted exchanges, can account for hundreds of thousands of transactions per second

I don't know what the safe minimum is, but at some point, Lightning channels must be opened and closed with some certain regularity: at some point, the base layer must absolutely begin scaling up to larger blocks or by using some other baselayer scaling mechanism. The necessity of channel opens and closes, at the very least, will require it.

By design, its expenses scale more slowly than its utility, due to its declining block subsidy that eventually results in a security model based only on transaction fees.

This is incorrect. Its subsidy is an artificial limit on its price, and thus also a limit on its energy consumption. Tangentially, the hashrate appears to also be a lower-end buffer on its minimum price.

Instead, I just consider proof-of-stake to be unsuitable for a democratized, decentralized, censorship-resistant global money

As a side note, since Lyn has been commenting on proof-of-stake and giving it significant coverage, I'll note that unfortunately all of the Ethereum PoS attack mitigations require an implied network-wide communications and cooperative surveillance. Disconnected clients become vulnerable immediately. Islands of connectivity are vulnerable. Based on current known research, there is nothing they can do to correct this, and there will always be the network isolation attacks to which Bitcoin is much, much less susceptible.

The problem with proof of stake is that there's nothing at stake. As far as current research goes, there is no current known way around this.