-

-

Save grantmcdermott/7d8f9ea20d2bbf54d3366f5a72482ad9 to your computer and use it in GitHub Desktop.

| # Context: https://twitter.com/grant_mcdermott/status/1487528757418102787 | |

| library(data.table) | |

| library(fixest) | |

| bboot = | |

| function(object, reps = 100L, cluster = NULL, ...) { | |

| fixest_obj = inherits(object, c('fixest', 'fixest_multi')) | |

| if (inherits(object, c('lm'))) { | |

| Ymat = object$model[, 1] | |

| } else if (fixest_obj) { | |

| Ymat = model.matrix(object, type = 'lhs', as.matrix = TRUE) | |

| } else { | |

| stop('\nModel or object class not currently supported.\n') | |

| } | |

| Xmat = model.matrix(object) | |

| n_weights = nrow(Xmat) | |

| fmat = NULL | |

| if (fixest_obj && !is.null(object$fixef_vars)) { | |

| fmat = model.matrix(object, type = 'fixef') | |

| } | |

| ## Have to do a bit of leg work to pull out the clusters and match to | |

| ## model matrix | |

| if (!is.null(cluster)) { | |

| if (inherits(cluster, "formula")) { | |

| cl_string = strsplit(paste0(cluster)[2], split = ' \\+ ')[[1]] | |

| } else { | |

| cl_string = paste(cluster) | |

| } | |

| if (!is.null(fmat) && all(cl_string %in% colnames(fmat))) { | |

| cl_mat = fmat[, cl_string] | |

| } else if (all(cl_string %in% colnames(Xmat))) { | |

| cl_mat = Xmat[, cl_string] | |

| } else { | |

| DATA = eval(object$call$data) | |

| if (all(cl_string %in% names(DATA))) { | |

| all_vars = sapply(list(Ymat, Xmat, fmat), colnames) | |

| if (inherits(all_vars, 'list')) all_vars = do.call('c', all_vars) | |

| all_vars = union(all_vars, cl_string) | |

| DATA = data.frame(DATA)[, intersect(colnames(DATA), all_vars)] | |

| DATA = DATA[complete.cases(DATA), ] | |

| cl_mat = model.matrix(~0+., DATA[, cl_string, drop=FALSE]) | |

| } else { | |

| stop(paste0('Could not find ', cluster, '. Please provide a valid input.\n')) | |

| } | |

| } | |

| if (!inherits(cl_mat, "matrix")) cl_mat = matrix(cl_mat) | |

| n_weights = nrow(unique(cl_mat)) | |

| ## Keep track of cluster id for consistent weighting within each | |

| ## cluster later on | |

| cl_mat = data.table::as.data.table(cl_mat) | |

| cl_mat$cl_id = data.table::frank(cl_mat, ties.method = "dense") | |

| } | |

| ## Pre-allocate space for efficiency | |

| wfits = matrix(0, reps, length(object$coefficients)) | |

| for (i in 1:reps) { | |

| if (is.null(cluster)) { | |

| weights = rexp(n_weights, rate = 1) | |

| } else { | |

| weights = cl_mat[, wt := rexp(1, rate = 1), by = cl_id][, wt] | |

| } | |

| ## Normalise weights | |

| ## (Unnecessary? https://twitter.com/deaneckles/status/1487506960698200067) | |

| # weights = weights / sum(weights) | |

| ## Demean X and Y matrices if fixed effects are present | |

| if (!is.null(fmat)) { | |

| Xmat = fixest::demean(X = Xmat, f = fmat, weights = weights) | |

| Ymat = fixest::demean(X = Ymat, f = fmat, weights = weights) | |

| } | |

| ## Fit weighted reg | |

| wfits[i, ] = lm.wfit(x = Xmat, y = Ymat, w = weights)$coefficients | |

| } | |

| colnames(wfits) = colnames(Xmat) | |

| class(wfits) = "bboot" | |

| ## Meta attributes | |

| attr(wfits, "coefs") = try(coefficients(object), silent = TRUE) | |

| attr(wfits, "df") = try(df.residual(object), silent = TRUE) | |

| attr(wfits, "se") = try(sqrt(diag(cov(wfits))), silent = TRUE) | |

| attr(wfits, "reps") = reps | |

| return(wfits) | |

| } | |

| # | |

| ## Methods | |

| # | |

| summary.bboot = function(object, level = 0.95, ...) { | |

| alpha = 1 - level | |

| lwr = alpha/2 | |

| upr = 1-lwr | |

| est = attr(object, "coefs") | |

| se = attr(object, "se") | |

| df = attr(object, "df") | |

| cnames = c("Estimate", "Std. Error") | |

| tval = as.vector(est)/se | |

| if (is.null(df)) df = 0 | |

| if (is.finite(df) && df > 0) { | |

| pval = 2 * pt(abs(tval), df = df, lower.tail = FALSE) | |

| fac = qt(alpha, df = df) | |

| cnames = c(cnames, "t value", "Pr(>|t|)") | |

| } else { | |

| pval = 2 * pnorm(abs(tval), lower.tail = FALSE) | |

| fac = qnorm(alpha) | |

| cnames = c(cnames, "z value", "Pr(>|z|)") | |

| } | |

| out = cbind(est, se, tval, pval) | |

| colnames(out) = cnames | |

| ci = cbind(est + fac * se, est - fac * se) | |

| colnames(ci) = c("Lower", "Upper") | |

| out = cbind(out, ci) | |

| # qtiles = t(apply(object, 2, \(x) c(mean(x), quantile(x, c(lwr, upr))))) | |

| # colnames(qtiles) = c("mean", "conf.low", "conf.upper") | |

| # attr(out, "quantiles") = qtiles | |

| out | |

| } | |

| print.bboot = function(object, ...) { | |

| out = summary(object, ...) | |

| cat("Bayesian bootstrap: Standard errors based on", attr(object, "reps"), "reps.", "\n\n") | |

| print(out, digits = 4, quote = FALSE, print.gap = 2L) | |

| } | |

| # | |

| ## Examples | |

| # | |

| set.seed(123) | |

| mod = lm(mpg ~ wt + hp, mtcars) | |

| bb_mod = bboot(mod, reps = 1e3) | |

| bb_mod | |

| hist(bb_mod[, 'wt'], | |

| breaks = 100, | |

| border = 'white', | |

| main = 'Bayesian bootstrap: wt') | |

| # Add cluster variables with a formula | |

| set.seed(42) | |

| bboot(mod, reps = 1e3, cluster = ~cyl) | |

| # Same result for fixest::feols (no FEs) | |

| set.seed(42) | |

| feols(mpg ~ wt + hp, mtcars) |> | |

| bboot(reps = 1e3, cluster = ~cyl) | |

| # Incl. FEs is fine too (although adds a bit of overhead) | |

| feols(mpg ~ wt + hp | cyl, mtcars, vcov = 'iid') |> | |

| bboot(reps = 1e3) | |

| # Can combine FEs and clustering as well | |

| feols(mpg ~ wt + hp | cyl, mtcars, vcov = ~cyl) |> | |

| bboot(reps = 1e3, cluster = ~cyl) |

Thanks @Oravishayrizi, yes please do.

Hi @grantmcdermott, here is the modified version of the summary function that (I think) replicates the summary output produced by Stata for the 'regular' bootstrap. (Obviously, Stata offers many modifications to this output)

First, I ran bootstrap estimation in Stata 16 and saved data from the different replications:

use http://www.stata-press.com/data/r16/auto, clear

bootstrap, reps(100) seed(1) ///

saving(C:\R\boot.dta, every(1) double replace): ///

regress mpg weight gear foreign

Then, I used this function to produce the same summary statistics.

summary.bboot = function(object, level = 0.95,lmobject, ...) {

alpha = 1 - level

sd.v=apply(object,2,sd)

z.v=coef(lmobject)/sd.v

pval.v=2*(1-pt(abs(z.v),Inf , lower.tail = TRUE))

out<-data.frame("Observed Coef."=coef(lmobject),

"Bootstrap_S.E."=sd.v,

"z"=z.v,

"p.val"=pval.v,

"lb"=coef(lmobject)-qt(p = 1-alpha/2,df=Inf,lower.tail = TRUE)*sd.v,

"ub"=coef(lmobject)+qt(p = 1-alpha/2,df=Inf,lower.tail = TRUE)*sd.v)

out<-round(out,6)

out$z<-round(out$z,2)

out$p.val<-round(out$p.val,3)

out}

I had to add the lmobject argument since Stata reports the observed coefficient (the value of the statistic calculated with the

original dataset) rather than the average of the estimated coefficients from the different draws.

The confidence interval seems to be calculated based on this formula:

(again, the coefficient is estimated using the original dataset)

I uploaded to rpubs.com a document containing the results from both Stata and R. here is the link

I hope that I am not misleading you or other users. Please take this with a grain of salt.

Or

Thanks very much @Oravishayrizi.

I'm a little bit confused, though. I think your Stata command is just implementing the standard bootstrap method (i.e. resampling rows with replacement). The bboot function that I've written above is the Bayesian bootstrap, which is based on re-weighting. See here. Also, I don't see why a parametric CI calculation should be used for the bootstrap. Isn't the point the point of the bootstrap to avoid the parametric restrictions (e.g. assumptions about normality)? I 'm looking very quickly at your code so apologies if I'm missing something!

Thanks again,

I read the tweet that you mentioned about the Bayesian bootstrapping. In fact, this is how I learn about it :). My understanding is that one can think of the Bayesian bootstrapping similarly to how I think of the re-sampling bootstrap, both in terms of usage and interpretation. Thus, I wanted to modify your summary function to look similar to Stata's (re-sampling) bootstrap command.

Lesson learned #1 - I guess I was too technical about bootstrapping. I never thought that once I use the usual confidence interval, I assume that the sampling is approximately normal, so thank you for highlighting that. However, I think that there are circumstances where this assumption is reasonable, and the use of the standard CI and p-values are handy.

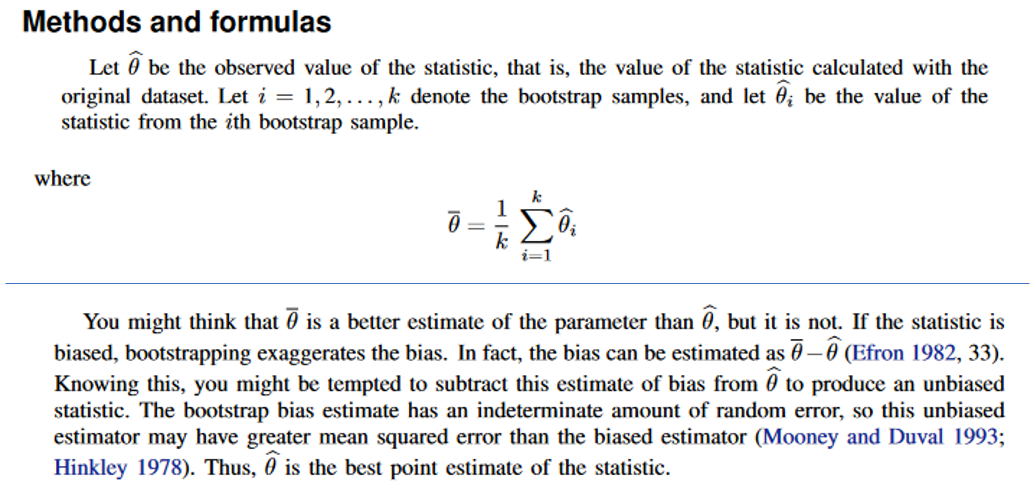

lesson learned #2 - Stata’s documentation notes that:

I'm not sure whether this holds for Bayesian bootstrap, but I'm highlighting it just in case you'd be interested.

Sources:

https://www.stata.com/manuals/rbootstrap.pdf#rbootstrap

https://www.stata.com/manuals/rbootstrappostestimation.pdf#rbootstrappostestimation

Hi again @Oravishayrizi. Sorry for the long delay between replies. Too many balls in the air...

I spoke to @zeileis about what he does for sandwhich::vcovBS and the short answer is just grab the standard Pearson correlation matrix (i.e. produced by applying cov() on all of the bootstrapped results). No small sample adjustments, which I think is reasonable, although there's been some discussion about what to do in the presence of few clusters.

Anyway, I've adjusted my original bboot function above to include an SE attribute based on this approach. It's very simple and just calls sqrt(diag(wfits)). The corresponding summary/print methods retrieve this attribute and prints it.

Also, since I'm now sticking to what sandwich and lmtest do now, I've also gone ahead and adjusted some other model statistics to be closer in line with your parametric suggestions. The default print method should be what you're looking for. I'm taking some lazy shortcuts, but really this is just a proof-of-concept until Achim or Laurent decide to role something like this into sandwich or fixest. (If not then I might do it for my own ritest package.)

You don't need to apologize.

Thank you very much for the detailed answer!

Hi Grant, thank you for this great resource!

I've noticed that Stata produces Confidence Interval differently from those computed by

summary.bboot.In addition, when running bootstrap in Stata, it also reports, by default, p-values for the estimation, rather than just CI.

Can I share with you a Stata script and a modified version of the function that replicates its results?